The Hidden Cost of DIY Bookkeeping for Law Firms

Data-Driven Insights on Legal Financial Management

According to the American Bar Association, 27% of attorney disciplinary actions stem from financial management issues, with trust account violations representing the leading cause. A 2024 Thomson Reuters Legal Financial Management Survey revealed that law firms using professional bookkeeping services reported 31% higher profit margins than those managing finances in-house, while the ABA's Legal Technology Survey found that 67% of solo and small firm attorneys spend between 5-10 hours weekly on administrative financial tasks—time worth $1,500-$3,000 at standard billing rates.

Most attorneys believe handling their own books saves money. The data suggests otherwise. Beneath the surface, hidden mistakes, overlooked compliance requirements, and misallocated time accumulate into substantial financial impact.

DIY bookkeeping appears strategic and cost-effective—particularly during a firm's early stages. However, what presents as a positive balance often conceals legal accounting mistakes, missed financial transactions, and client trust account fund violations capable of triggering significant financial penalties.

This law firm accounting guide examines the actual cost of DIY bookkeeping and presents a more strategic approach. From ethics rules violations and improper operating account management to cash basis accounting misinterpretations and inadequate financial forecasting—here's what sophisticated attorneys should consider before reopening QuickBooks.

Why Law Firm Accounting Is Essential for Financial Health

Law firm accounting forms the foundation of your firm's financial health. It provides the structure for legal professionals to manage financial transactions, allocate incurred costs with precision, and maintain compliance with legal accounting rules governing trust accounts, financial reporting, and business bank accounts.

Trust Accounting Defined

Trust accounting governs how law firms hold, track, and report client funds — and it's one of the most scrutinized areas in legal compliance. Every dollar must be assigned to the correct client ledger, reconciled monthly, and isolated from operating accounts. These aren’t accounting preferences — they’re ethical mandates. And when trust accounting fails, careers follow.

Most law firms benefit substantially from the disciplined separation of personal and business expenses, strategic use of business savings accounts and business checking accounts, and proper maintenance of firm-wide financial accounts. This structure creates a competitive advantage in managing firm's finances. Without this foundation, law firms risk violating legal accounting rules, facing unsuccessful audits, and falling behind on tax obligations.

Why DIY Bookkeeping Feels Cheaper — But Costs Law Firms More

Many attorneys take pride in self-sufficiency. Having built your firm from inception, handling your books appears to be simply another executive function. But law firm bookkeeping isn't merely another operational task—it's a sophisticated financial management function with direct impact on your firm's accounting and legal compliance posture.

The disciplined separation of personal and business expenses remains non-negotiable. When attorneys co-mingle funds, operate without proper business bank accounts, or incorrectly classify legal services revenue, they expose themselves to tax examinations, ethics violations, and compromised financial statements. This isn't fiscal responsibility—it's creating the conditions for financial disorder in your firm's finances.

Time dedicated to manual financial data tracking, client ledger reconciliation, or approximating your law firm's financial health directly reduces billable capacity. More critically, DIY bookkeeping frequently leads to overlooked accounts payable, understated revenue, and suboptimal use of legal accounting software—all of which constrain growth potential.

7 Costly Bookkeeping Mistakes Law Firms Make Without Realizing It

Even meticulously organized law firms remain vulnerable to critical financial missteps when managing books internally. Without specialized training in legal bookkeeping, most legal professionals underestimate the complexity behind tasks like trust reconciliation, proper expense categorization, and maintaining audit-ready financial records.

It’s not about intent — it’s about structure. Attorneys relying solely on their software often assume performance is adequate because the balances appear correct. But software doesn’t detect incorrectly logged financial transactions, blurred lines between client costs and overhead, or unreconciled lawyers’ trust accounts. These gaps aren’t just technical errors — they’re compliance risks with real consequences.

Core bookkeeping tasks like client ledger maintenance, matter-specific tracking, and timely reconciliation must operate within a deliberate accounting practice, not as a reactive checklist. Monthly alignment between your bank statements, trust account balance, and client-level ledgers is the foundation of compliant bookkeeping — and one that even seasoned firms struggle to maintain without a legal-specific accounting service.

Trust account balances not reconciled monthly

Misclassified income and expenses

Personal and business funds mixed inappropriately

Late or inaccurate 1099 filings

Missed tax deductions

Uncollected AR due to insufficient tracking

No backup or audit trail for financial records

DIY law firm bookkeeping costs: $19,500 lost billable time, $13,000 accounting errors, $22,000 compliance risks - data from ABA survey

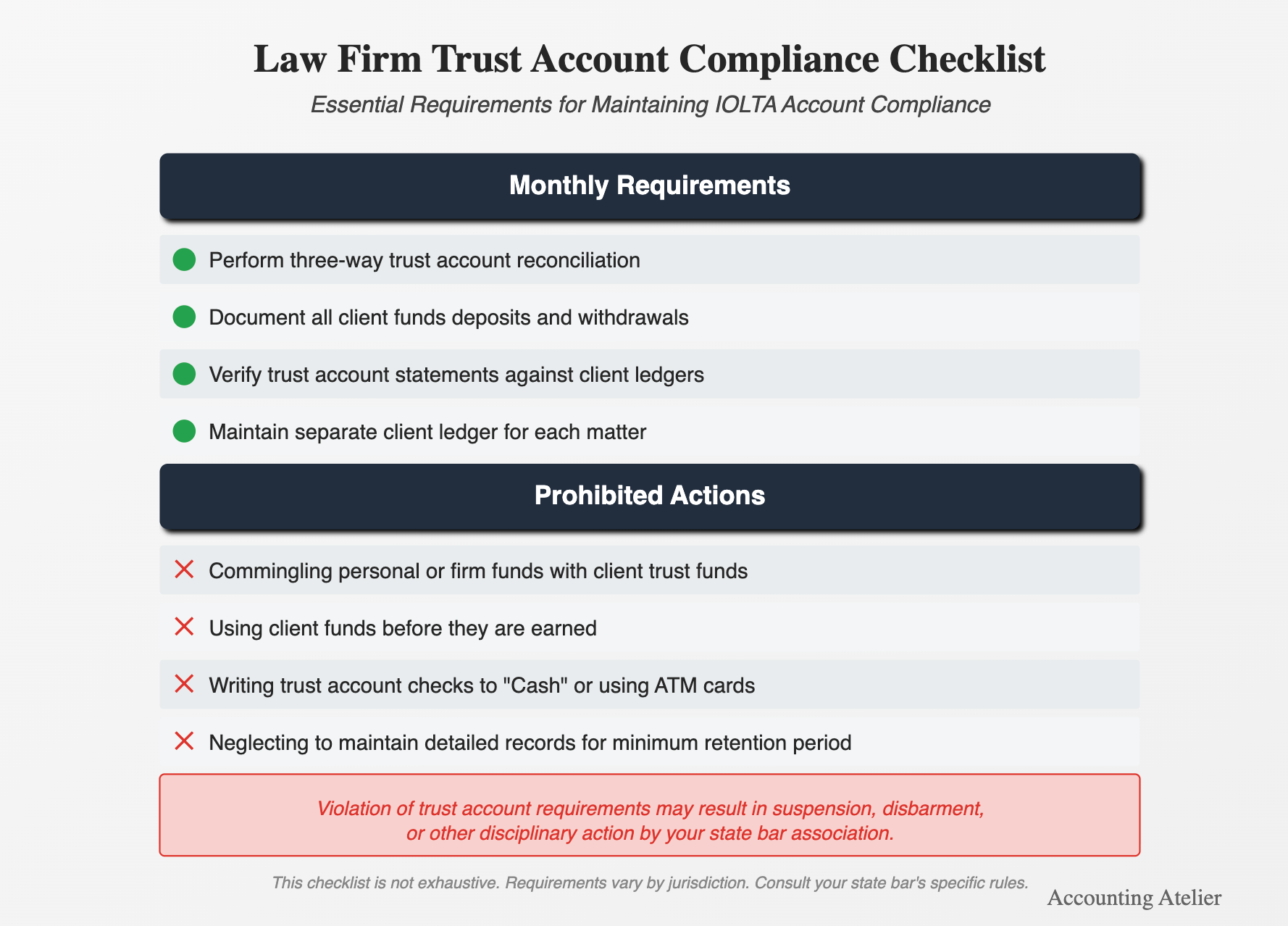

Trust Account Compliance: What Law Firms Can’t Afford to Overlook

Trust accounts aren’t just another category in your books — they’re a regulatory risk zone with zero margin for error. Every jurisdiction enforces strict legal accounting rules, and even a single misstep in how a financial transaction is recorded can trigger disciplinary action, audits, or disbarment.

Many small law firms rely on DIY workflows or standard business software to manage client funds, assuming that a positive balance means compliance. But tools like Clio accounting, QuickBooks, and Xero don’t enforce bar standards — they simply record what’s entered. Without a deliberate, compliance-driven accounting practice, the risk compounds.

These systems are not substitutes for expertise. Whether you're a solo attorney or managing partner, what protects your firm isn’t the software — it’s the process behind it. And that process demands an experienced accounting service tailored for legal professionals, built around IOLTA, audit trails, and jurisdictional rules.

The Non-Negotiable: Three-Way Trust Account Reconciliation

Under ABA Model Rule 1.15 and its state equivalents, law firms must complete a three-way reconciliation of their trust accounts monthly. This means confirming exact agreement between:

The trust bank statement

The total of all client funds held in trust

The internal trust account book balance

If these three records don’t match — even by a few dollars — your compliance is already compromised.

Legal-specific platforms like PCLaw, Tabs3, or CosmoLex offer built-in reconciliation modules. But without proper configuration, even these tools can fail to prevent violations. Generic accounting solutions like QuickBooks require significant customization to meet legal standards, especially for firms managing multiple client matters and operating under accrual accounting.

Why DIY Systems Put Your License at Risk

Most trust account violations aren't malicious — they're the product of incomplete records, manual data entry, or inconsistent workflows. Common breakdowns include:

Failure to maintain individual ledgers for each client

Missing monthly reconciliations

Commingling of operational and trust funds

Inadequate legal bookkeeping systems to document transactions

Improper retainer handling or premature disbursement of unearned fees

Even sophisticated firms aren’t immune. Without legal-specific internal controls, it’s easy for issues to compound unnoticed until they surface during an audit.

A Strategic Case for Professional Oversight

Bringing in a legal-specific bookkeeping service is about more than risk reduction — it's about building lasting infrastructure inside your financial operations. In the legal profession, where ethical compliance and client transparency are non-negotiable, proper systems aren't optional — they're foundational.

High-level support includes:

Documented, monthly three-way trust reconciliations

Client billing workflows tied directly to matter-level reporting

Retainer handling protocols that align with bar-reviewed billing practices

IOLTA interest disbursement oversight

Accurate bookkeeping processes with audit-ready documentation

Active coordination across matter management, tax reporting, and cash flow

Experienced legal bookkeepers go beyond categorization — they implement systems that support effective bookkeeping across every layer of your firm. Their work reinforces the principles behind strong legal accounting practices and eliminates the inefficiencies that cost time, revenue, and compliance status.

Firms that continue relying on general accounting firms, spreadsheets, or part-time internal support often fail to detect foundational issues until they surface during audits. For many firms, the better path is outsourcing bookkeeping to specialists who understand what legal compliance really demands. Your trust account should never be a liability — it should be a testament to your firm's standards.

Why Most Law Firms Struggle With Financial Reporting

Financial reporting transcends basic revenue recognition. It requires interpreting what numbers reveal about your law firm's financial health, performance metrics, and compliance position. Suboptimal financial processes typically result in incomplete financial data, inaccurate tax documentation, or misunderstood cash flow dynamics.

DIY bookkeeping rarely incorporates structured preparation of financial statements. Without consistent reporting—income statements, balance sheets, and trust liability summaries—your firm operates without vital intelligence. This prevents accurate accounts receivable tracking, strategic tax planning, or data-driven business decisions based on reliable financial records.

The Financial Risks Lurking Behind DIY Systems

DIY bookkeeping exposes your practice to financial vulnerabilities you may not have evaluated. A single trust account mistake can trigger IOLTA violations—potentially initiating ethics investigations or disbarment proceedings. Inaccurate expense categorization can misrepresent your firm's taxable income, creating exposure to audits or payment deficiency penalties.

Accrual accounting, which documents revenues and expenses at the point they're earned or incurred rather than when cash transfers occur, provides essential structure for law firms. This methodology delivers accurate understanding of the firm's true financial position, though it introduces complexities not present in cash accounting systems.

When bookkeeping is performed internally without specialized expertise, the reports guiding your decisions may contain fundamental flaws. Cash basis accounting statements often create profit illusions while disregarding unpaid invoices and upcoming obligations. These information gaps make confident business decisions about your firm's finances nearly impossible—and create unnecessary tax season complications.

IOLTA compliance checklist for attorneys: monthly trust reconciliation requirements and prohibited actions that risk disbarment - required by state bar associations

How Legal Accounting Differs from Traditional Small Business Bookkeeping

Legal accounting represents a specialized discipline, not a general business function. Unlike standard businesses, law firms operate under legal accounting rules that vary by jurisdiction. Client funds management extends beyond deposit documentation—it requires producing audit-ready reports, maintaining precise client ledger balances, and establishing complete separation between trust and operating accounts.

Even with sophisticated law firm accounting software, these systems remain dependent on the expertise of the individual managing the data. They provide no inherent protection against common legal accounting mistakes such as fund commingling or inaccurate financial statements. Legal bookkeeping demands precision, specialized training, and comprehensive understanding of a law firm's accounting process.

Legal-Specific Chart of Accounts Structure

Law firms require specialized account structures that standard business bookkeeping doesn't address:

Matter-Centric Accounting: Tracking profitability by practice area and individual matter

Trust Account Liability Tracking: IOLTA and non-interest-bearing trust accounts

Advanced Retainer Management: Earned and unearned fee distinctions

Cost Recovery Systems: Client-billable vs. firm overhead expense tracking

Allocation Methodologies: Partner compensation and profit distribution tracking

Legal accounting software like ActionStep, Soluno, and TimeSolv offers legal-specific chart of accounts templates, but the implementation requires specialized expertise to align with your firm's practice areas, partnership structure, and compensation methodology.

Managing Bookkeeping Tasks With Legal Accounting Software

Legal accounting software platforms like QuickBooks Online and Clio Manage streamline many processes but don't eliminate the need for expert oversight. Your firm still requires qualified professionals to reconcile bank accounts, monitor accounts payable, and maintain the firm's finances through properly configured financial management software systems.

Firms frequently overestimate automation's protective capabilities. Without active management by qualified specialists, these tools can't prevent financial statement preparation errors, business expenses misclassification, or ethics rules violations related to client fund management. Accounting software provides a framework—not a replacement for strategic expertise and professional skill in managing financial processes.

From DIY to Delegation: What Changes With Monthly Retainer Bookkeeping

Engaging a legal bookkeeping specialist isn't merely task delegation—it represents a strategic upgrade to your financial infrastructure. An experienced professional manages all financial accounts, maintains compliance with legal accounting rules, and provides your leadership team with real-time visibility into cash flow, accounts receivable, and the firm's financial performance metrics.

You'll operate with the confidence that comes from knowing your operating account maintains appropriate separation, your lawyers trust accounts meet compliance standards, and your business accounts undergo monthly reconciliation. This structure facilitates better strategic decisions, efficient collections, and reduced administrative pressure related to your firm's financial accounts.

Professional bookkeeping transforms from cost center to value driver. Your financial operations become a growth asset rather than a liability. Most significantly—you fully assume your role as a law firm principal rather than remaining constrained by back-office financial record management.

Implementation Timeline: Transitioning to Professional Law Firm Bookkeeping

Phase 1: Discovery & Assessment (Weeks 1-2)

Comprehensive financial systems audit

Trust account compliance review

Chart of accounts analysis and restructuring

Current software assessment and integration planning

Financial reporting gap analysis

Phase 2: Infrastructure Development (Weeks 3-4)

Implementation of legal-specific accounting architecture

Chart of accounts refinement for practice area tracking

Trust accounting system configuration

Integration of practice management and accounting software

Documentation of firm-specific accounting protocols

Phase 3: Operational Implementation (Months 2-3)

Transition of day-to-day bookkeeping operations

Implementation of three-way trust reconciliation processes

Financial reporting dashboard development

Staff training on documentation and communication protocols

Establishment of monthly financial review cadence

Phase 4: Optimization & Strategic Advisory (Month 4+)

Comparative financial performance analysis

Cash flow optimization strategies

Tax planning integration

Financial efficiency ratio improvements

Growth forecasting and expansion modeling

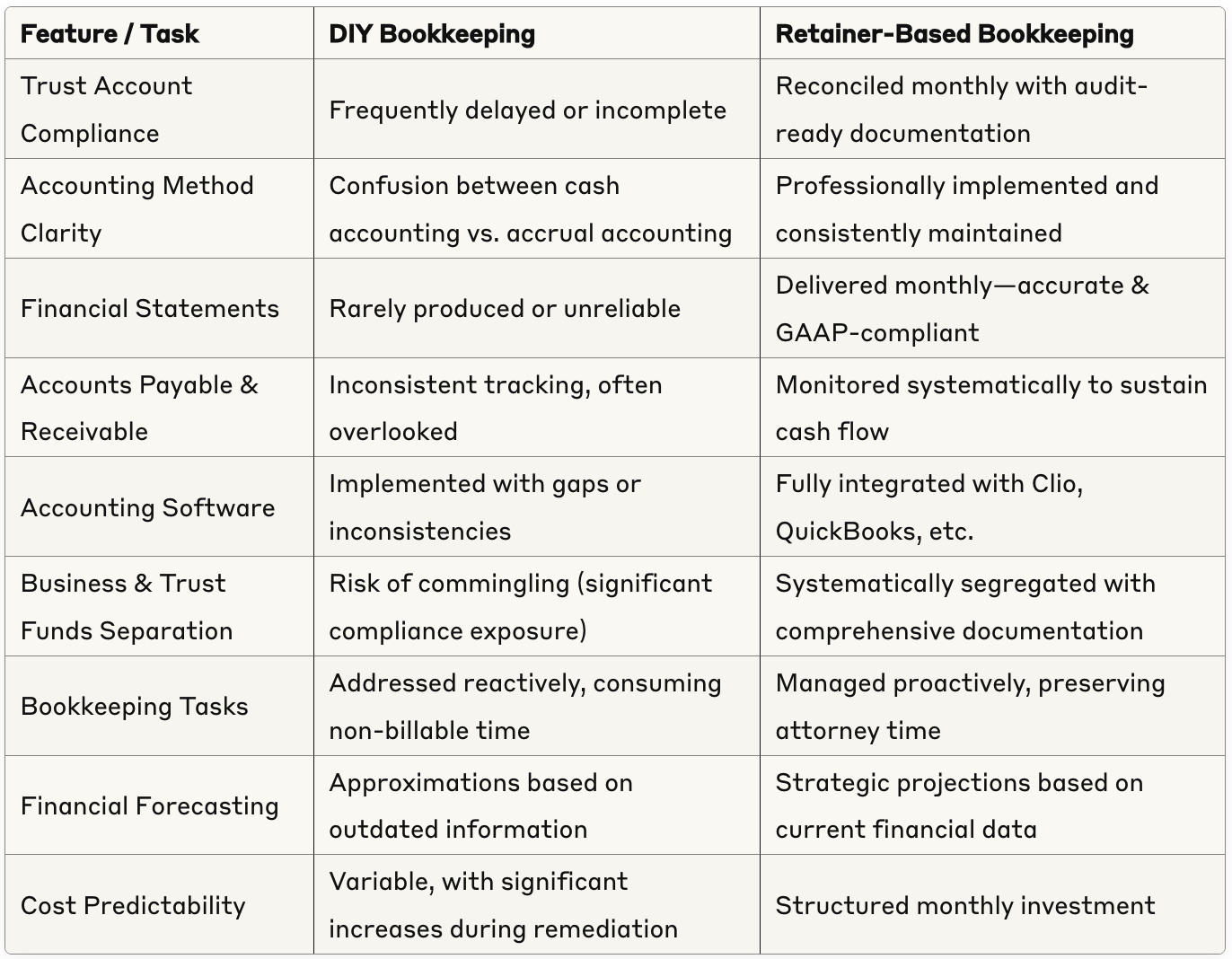

DIY vs. Retainer-Based Bookkeeping for Law Firms

How Clean Law Firm Books Save Time, Money, and Compliance Headaches

Retainer-based bookkeeping provides your firm with the financial architecture needed for strategic growth. Rather than addressing issues reactively, you receive monthly support with properly maintained books, reconciled accounts, and proactive communication. With predictable pricing, you eliminate the cost spikes associated with last-minute financial remediation.

Consistent, professional bookkeeping establishes the foundation for accurate tax filing and compliance, allowing your law firm to maintain consistent accounting methodology and avoid potential complications with tax authorities. Multiple payment methods receive proper tracking and documentation under this approach.

You reclaim valuable time—quantifiable, productive time—to focus on client representation. No more late-night reconciliations or uncertainty about which expenses covers incurred costs. With professional retainer support, your financial operations transform into a strategic asset rather than an administrative burden.

The Real Cost of Doing Bookkeeping In-House at Your Law Firm

When you bill at $300/hour and devote five hours monthly to bookkeeping functions, you're sacrificing $1,500 in billable capacity. Yet this represents only the beginning. Overlooked deductions, inadequate forecasting, delayed tax payments, and unrecognized AR collectively impact your law firm's financial health.

DIY bookkeeping elevates your exposure to legal accounting rules violations, client funds mismanagement, or inconsistent application of your firm's accounting method. Post-facto remediation invariably costs substantially more than proactive monthly services that maintain proper financial discipline from the outset for your firm's finances.

Conclusion: You Built a Law Firm — Not a Side Hustle

You didn't invest in legal education and build a practice to manually track bank balances, categorize business expenses, or monitor accounts receivable. Yet DIY bookkeeping constrains you to precisely these functions. It positions you in a reactive posture rather than enabling strategic growth.

Clean books. Accurate financial records. Audit-ready trust accounts. Strategic financial statements. When your financial systems deliver these foundational elements—you position your law firm for business growth rather than merely sustaining a practice.

When you're prepared to delegate financial operations and accelerate growth, we're positioned to implement a sophisticated legal accounting process tailored to your firm.

Contact us today!

FAQ – Bookkeeping for Law Firms

Q: Is it really that risky to do my own bookkeeping? Yes. Most law firms underestimate the legal, financial, and compliance exposures involved. A single error in trust account management, tax documentation, or business expense classification can trigger audits, ethics reviews, or significant financial penalties.

Q: Can't my office manager handle it? Unless they possess specific training in legal accounting and specialized knowledge in managing client trust account funds, no. This isn't standard administrative work—it's specialized financial oversight requiring detailed understanding of legal accounting rules.

Q: What does monthly retainer bookkeeping include? Complete reconciliations, financial statements, accounts payable and receivable oversight, tax planning support, legal compliance monitoring, and additional services. This represents comprehensive financial architecture—not basic transaction recording.

Q: What accounting software should law firms use? QuickBooks Online integrated with Clio Manage provides a robust foundation—but without qualified professional oversight, software alone cannot prevent cash flow challenges, trust violations, or audit exposure. Proper law firm accounting software selection and implementation remain essential.

Q: How much should law firms expect to pay? Most firms invest $500–$1,500 in monthly outsourced bookkeeping depending on complexity and scale. This represents a fraction of what you're likely losing through billable time inefficiency, process gaps, and tax optimization opportunities.

Q: How does bookkeeping differ across practice areas? Each practice area presents distinct accounting requirements. Personal injury firms need advanced settlement tracking and contingency fee calculations. Estate planning practices require intricate trust fund management. Family law practices need sophisticated retainer management. Litigation firms demand detailed expense allocation across matters. Your bookkeeping system must align with your specific practice area requirements.

Q: What are the IOLTA compliance requirements I should be most concerned about? The most critical IOLTA compliance requirements include: (1) Complete separation between earned and unearned fees; (2) Timely three-way monthly reconciliations with proper documentation; (3) Accurate client ledger maintenance showing all transactions by matter; (4) Immediate correction of any reconciliation discrepancies; (5) Proper handling of credit card payments to prevent commingling; and (6) Accurate tracking of interest accrued and remitted to the appropriate IOLTA program.

Q: How frequently should law firms generate financial reports? Sophisticated law firms require monthly financial reporting packages including P&L statements, balance sheets, trust liability summaries, accounts receivable aging reports, and matter profitability analyses. Quarterly more comprehensive financial reviews should examine key performance indicators, partner compensation metrics, and growth trajectory analyses. Annual strategic financial planning should incorporate tax optimization strategies, capital investment evaluation, and comprehensive firm valuation metrics.