Legal Bookkeeping for Law Firms: The IOLTA Compliance Guide Every Serious Attorney Needs in 2025

Legal Bookkeeping for Law Firms: The IOLTA Compliance Guide Every Serious Attorney Needs in 2025

You Didn’t Start a Law Firm to Worry About Your Books

On a Tuesday morning, a managing partner logs into QuickBooks.

The trust account doesn’t match the client ledger. Again.

That quiet, familiar dread creeps in - “I’ll figure it out before tax season.”But the calendar keeps moving. The records stay messy. The pressure builds.

This isn’t laziness. This is a law firm trying to stay afloat in a system that was never built for legal bookkeeping.

You didn’t go to law school to manage ledgers, reconcile IOLTA accounts, or figure out how to classify trust retainers.

This guide is here to give you back your time, protect your license, and finally make your firm’s financials match your level of excellence by addressing the unique challenges of accounting for law firms.

TL;DR – Law Firm Bookkeeping Isn’t About Tracking Expenses. It’s About Protecting Your Reputation.

You manage client money, not just firm money.

Your books must be ethically compliant, audit-ready, and client-transparent.

Most CPAs and generalist bookkeepers aren’t trained for legal trust accounting.

IOLTA compliance isn’t optional - it’s a bar rule.

The wrong system won’t just cost you time. It could cost you your license.

IOLTA accounts must have strict rules to prevent borrowing from them or commingling client funds with the lawyer's business funds.

Let’s fix it—properly.

Understanding Law Firm Accounting

What is law firm accounting?

Law firm accounting is the specialized process of managing a law firm’s financial transactions, including client funds, trust accounts, and business expenses. Unlike general business accounting, it requires meticulous tracking and categorization of every dollar to ensure compliance with legal and ethical standards. This involves recording, classifying, and reporting financial information accurately to meet regulatory requirements and support informed business decisions. Effective law firm's accounting safeguards client funds, maintains trust account integrity, and ensures that the firm’s financial records are both accurate and compliant.

Why is accounting important for law firms?

A law firm's accounting is the backbone of financial transparency, compliance, and profitability. It plays a crucial role in managing client funds, tracking billable hours, and making strategic business decisions. Accurate accounting practices help law firms maintain good relationships with clients by ensuring clear and precise financial reporting. Additionally, it aids in managing cash flow, planning for taxes efficiently, and avoiding costly errors and penalties. By adopting best practices in accounting, law firms can enhance their financial performance, reduce risks, and bolster their reputation within the legal industry.

Why Law Firm Bookkeeping Is a Different Beast

1. You're Managing Client Funds, Not Just Business Revenue

When a client gives you a retainer, that money doesn’t belong to you—not yet. Every financial transaction must be tracked, protected, and reconciled. Trust funds held in an IOLTA account are not considered the lawyer’s funds until earned fees are withdrawn. Law firms must make sure that all funds in trust accounts are earned before withdrawing them for operation expenses. Additionally, any interest earned on IOLTA accounts is sent to the state bar for charitable purposes.

If it sits in the wrong account or gets mis-categorized as income, you’re in dangerous territory.

2. Your Trust Account Is Under Legal Scrutiny

A trust account isn’t just another bank account—it’s a fiduciary commitment. Financial statements play a crucial role in maintaining accurate and compliant accounting practices for law firms. One error in your trust ledger, one unreconciled transaction, one untracked retainer—and you’ve exposed yourself to ethics violations and bar complaints. Trust accounting requires law firms to keep meticulous records of all transactions in each client’s trust account.

3. Traditional Accounting Doesn’t Apply

Standard business rules don’t apply here. You’re not just running payroll or managing vendor payments. Cash basis accounting, often used by law firms for its simplicity, records revenues and expenses only when cash transactions occur. You’re navigating the intersection of finance, compliance, and the law.

Legal bookkeeping isn’t harder—it’s higher stakes, and efficient management of a law firm's accounting system is crucial for compliance and financial success.

Setting Up Your Law Firm’s Finances

Choosing the right bank account for your law firm

Selecting the right bank account is a pivotal step in setting up your law firm’s finances. Law firms need to maintain separate bank accounts for client funds, business expenses, and trust accounts to ensure compliance and financial integrity. It’s essential to choose a bank that offers specialized services tailored to law firms, such as IOLTA accounts, trust accounting, and comprehensive financial reporting.

When evaluating banks, consider factors like fees, interest rates, customer service, and security measures. A bank that understands the unique needs of law firms can provide the tools and support necessary to manage your financial transactions securely and compliantly, ensuring your firm's accounting and financial management are robust and reliable.

Opening a Business Bank Account

Opening a business bank account is a crucial step for law firms to manage their finances effectively. A business bank account helps law firms to keep their personal and business finances separate, which is essential for maintaining accurate financial records and complying with tax laws. When opening a business bank account, law firms should consider the following factors:

Fees: Look for a bank that offers low or no fees for business accounts. Hidden fees can add up quickly, impacting your firm’s cash flow.

Interest Rates: Consider a bank that offers competitive interest rates on business savings accounts. This can help your firm earn a return on idle funds.

Customer Service: Choose a bank with excellent customer service and support. Having a reliable point of contact can make managing your accounts smoother.

Online Banking: Ensure the bank offers robust online banking services that allow you to manage your accounts, pay bills, and transfer funds easily. This convenience is essential for busy law firms.

Security: Consider a bank with robust security measures to protect your accounts and data. Cybersecurity is paramount in today’s digital age.

By carefully selecting a bank that meets these criteria, law firms can ensure their financial transactions are handled efficiently and securely, supporting their overall financial management strategy.

Setting Up Separate Accounts for Client Funds

Law firms are required to maintain separate accounts for client funds to ensure compliance with trust accounting regulations. Setting up separate accounts for client funds helps law firms to keep client funds separate from their business finances, which is essential for maintaining accurate financial records and complying with tax laws. When setting up separate accounts for client funds, law firms should consider the following factors:

IOLTA Accounts: Consider setting up an IOLTA (Interest on Lawyer Trust Account) account to earn interest on client funds. The interest generated is typically used for charitable purposes, benefiting the community.

Trust Accounting Software: Use trust accounting software to manage client funds and ensure compliance with trust accounting regulations. Legal accounting software can automate many of the complex tasks involved in trust accounting.

Separate Accounts for Each Client: Set up separate accounts for each client to ensure that client funds are kept separate and accurate. This practice helps in maintaining transparency and avoiding any commingling of funds.

Regular Reconciliation: Regularly reconcile client accounts to ensure accuracy and compliance. Monthly reconciliations can help identify discrepancies early and maintain the integrity of your trust accounting.

By implementing these practices, law firms can manage client funds responsibly, ensuring compliance with legal standards and maintaining client trust.

Accounting Methods for Law Firms

Law firms can choose from two main accounting methods: cash basis accounting and accrual accounting. Each method has its advantages and disadvantages, and law firms should consider their specific needs and circumstances when choosing an accounting method.

Cash Accounting vs. Accrual Accounting

Cash basis accounting recognizes revenues and expenses when cash is received or paid, whereas accrual accounting recognizes revenues and expenses when earned or incurred, regardless of when cash is received or paid.

Cash Basis Accounting: This method is simpler and easier to manage. It provides a clear picture of cash flow, making it easier to see how much cash is available at any given time. However, it may not provide an accurate picture of a law firm’s financial performance over time, as it doesn’t account for money that is owed but not yet received or expenses that have been incurred but not yet paid.

Accrual Accounting: This method provides a more accurate picture of a law firm’s financial performance, as it matches revenues with the expenses incurred to generate them. It can be more complex and require more accounting expertise, but it offers a better long-term view of the firm’s financial health.

Which Method is Right for Your Law Firm?

The choice of accounting method depends on the specific needs and circumstances of the law firm.

Cash Basis Accounting: Law firms with simple financial transactions and few assets may prefer cash basis accounting. It’s straightforward and easier to manage, making it suitable for smaller firms or those with less complex financial activities.

Accrual Accounting: Law firms with complex financial transactions and multiple assets may prefer accrual accounting. This method provides a more comprehensive view of the firm’s financial health, which is crucial for larger firms or those with significant financial activities.

Law firms should consult with a certified public accountant (CPA) or accounting expert to determine the best accounting method for their specific needs. By choosing the right method, law firms can ensure accurate financial reporting and better financial management.

What Does a Bookkeeper Actually Do for a Law Firm?

A legal-focused bookkeeper is not a data-entry clerk. They’re your first line of financial defense.

Here’s what they handle:

Categorizing every transaction properly

Managing and reconciling IOLTA trust accounts monthly

Tracking client retainers and separating earned from unearned income

Maintaining audit-proof ledgers for each client

Keeping business and trust funds fully segregated

Collaborating with your CPA to prepare clean year-end financials

Identifying compliance gaps before they become violations

Utilizing financial reports to make informed business decisions

Without a trained bookkeeper who knows how to do all of this, your financial system is a liability. With one? You gain clarity, control, and confidence.

What IOLTA Compliance Actually Requires

This Isn’t “Close Enough” Accounting

You don’t “sort of” comply with bar regulations. You either do—or you don’t.

That’s what makes IOLTA trust account management so high stakes.

Here’s what true IOLTA compliance looks like:

Every client’s funds are stored in a separate trust account or properly tracked via individual client ledgers

Monthly three-way reconciliations between the trust ledger, bank statement, and client ledger balances

Trust money is never co-mingled with operating funds

Earned vs. unearned income is tracked and transferred properly

Reimbursements, court fees, and third-party payments are logged with audit-ready clarity

A three-way reconciliation is essential for law firms to ensure accuracy and compliance in their trust accounting. All lawyers must complete at least quarterly three-way reconciliations of their trust accounts to ensure compliance.

If your system can’t do that—your books are not compliant. And the bar doesn’t care how busy your firm is.

Is QuickBooks Good for Lawyers?

The short answer: Only if it’s set up by someone who understands legal bookkeeping and the importance of law firm accounting software.

What QuickBooks can do:

Track transactions across multiple accounts

Reconcile bank accounts monthly

Categorize expenses

Generate custom reports

What it won’t do on its own:

Set up proper trust account workflows

Create client-specific ledgers for IOLTA

Alert you if you're violating bar rules

Prevent you from making compliance-killing errors

QuickBooks is like a scalpel. In the hands of a surgeon, it saves lives.

In the hands of someone who doesn’t understand IOLTA? It cuts your firm open and leaves you exposed.

The Hidden Costs of Getting This Wrong

1. Bar Complaints and Ethical Violations

A single audit showing funds weren’t tracked properly? That’s a risk to your license.

2. Clients Losing Trust in You

Delayed refunds. Reimbursement errors. Unclear payment tracking. These erode the professional image you’ve worked hard to build.

3. Wasted Billable Hours

The time you or your staff spend untangling transactions is time not spent billing, serving, or growing. Period. Accurate bookkeeping and a well-maintained firm's accounting system help law firms avoid missing billable hours and ensure timely invoicing, which directly impacts the firm’s financial health. Law firms must monitor cash flow carefully to ensure they have sufficient funds for operational expenses and client costs. Additionally, law firms should track revenue and expenses separately to maintain clear financial records.

4. Lost Profit

Misclassified expenses. Missed deductions. Poor cash flow visibility. These mistakes cost firms thousands—quietly, over time. Setting a budget for the firm is the foundation of effective financial management and helps achieve financial goals. A business savings account is crucial for storing funds set aside for taxes and emergencies. Establishing a budget allows law firms to set expectations on cash flow and expenses. Tracking tax deductions throughout the year can ease the burden during tax season and potentially maximize returns. Setting a budget also helps law firms set revenue benchmarks and manage cash flow expectations.

5. Tax Season Panic

If you’re scrambling in March, your system failed you in September.

Common Bookkeeping Mistakes Law Firms Can’t Afford

1. Commingling Client Funds with Operating Income

This is the fastest way to violate IOLTA rules. Even a small mix-up—intentional or not—can put your license at risk.

2. Skipping Monthly Trust Reconciliations

A single unreconciled transaction may go unnoticed for months, and by the time it’s discovered, you’re facing an audit trail that doesn’t add up.

3. Relying on a CPA for Daily Bookkeeping

Most CPAs don’t touch your books until tax time. That’s 11 months of silence and unchecked exposure.

4. Using Software Without Legal Configuration

QuickBooks, Xero, or other tools don’t come out of the box with legal compliance built in. Without customization, they mislead more than they help. Law firms should set up a dedicated operating account to manage business expenses and ensure compliance with legal accounting standards. Using robust accounting software helps streamline law firm accounting tasks and ensures compliance.

Cloud-based accounting software automatically updates and backs up financial records. Automated accounting solutions reduce the risk of human error in law firm financial management. Implementing legal accounting software also allows firms to effectively monitor cash flow, ensuring financial stability. Notably, 28% of legal professionals use legal accounting software instead of consumer accounting software. Law firms may need to employ specific accounting methods based on annual revenue and operational needs.

5. Delegating to In-House Staff Who Don’t Understand Compliance

A receptionist or office manager may be smart—but without legal accounting training, they could unknowingly create costly errors. It's essential to hire accounting professionals with experience working with law firms to meet specific needs. Establishing internal controls within financial management can prevent fraud and ensure ethical practices.

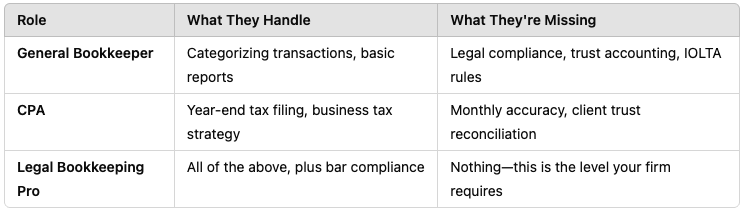

Comparison: Bookkeeper vs. CPA vs. Legal Bookkeeping Pro

What a Best-in-Class Law Firm Bookkeeping System Looks Like

Monthly reconciliation of every account—including all trust ledgers

A chart of accounts built specifically for legal accounting needs

Crystal-clear tracking of client retainers, unearned income, and trust disbursements

System-generated reports that show your firm’s financial health in real time

Full compliance with bar association rules, built into your process—not added after the fact

Double-entry accounting ensures a clear separation between a law firm’s financial transactions and client transactions

Effective law firm's accounting practices to maintain accurate and compliant financial records

This is the difference between “managing books” and running a practice that protects itself financially and legally.

The Real Problem Isn’t Bookkeeping. It’s System Failure.

You’ve built a firm. You’ve served clients. You’ve won hard cases.

But your books? They still feel like a black hole.

That’s not because you’re careless. It’s because you’ve been forced to juggle too many roles without the right financial infrastructure.

The problem isn’t QuickBooks. It’s who set it up.

The problem isn’t your CPA. It’s that they show up once a year.

The problem isn’t you. It’s the system. Employing outside help can free up time for lawyers to focus more on practicing law than managing finances. Regular financial analysis can help identify profitable areas of the business and inform strategic decisions. Accountants can help law firms with financial analysis, strategic planning, and compliance with legal regulations. Regular financial reporting provides insights that help law firms make data-driven decisions for growth. Additionally, 46% of legal professionals who use legal accounting software save 1-5 hours each week.

Imagine a Better Reality

You open your financial dashboard and everything is exactly where it should be.

The numbers make sense. The ledgers are current. The trust account is balanced—every client, every matter, every dollar accounted for.

You don’t wonder if your IOLTA records are audit-ready—you know they are.

You're not preparing for tax season at the last minute. You’ve been ready for months.

You no longer carry the quiet burden of uncertainty about your firm’s financial health.

You’re no longer one surprise away from hours of cleanup or awkward calls to your CPA.

Instead, you have clarity. You have structure. You have a system that keeps up with the speed and complexity of your practice.

This is what it feels like when your bookkeeping isn’t just “handled”—it’s working for you.

It supports your growth. It safeguards your license. It elevates your confidence in every business decision you make.

This isn’t just a clean set of books. This is operational peace.

This is what law firm owners deserve—and rarely get.

That’s what we deliver.

Let’s Clean This Up- And Rebuild It Right

If you’ve read this far, you already know something’s not working.

Maybe you’ve been patching together reports. Maybe your trust account gives you anxiety. Maybe your books feel like a house of cards that hasn’t fallen—but could.

This is your chance to stop reacting and start building the kind of financial system your firm actually needs.

Let’s set up a bookkeeping infrastructure that’s clean, compliant, and built to scale with you.

Let’s finally eliminate the friction, confusion, and risk that’s been following you for too long.

We don’t offer generic services. We partner with serious law firm owners to install systems that give them back control, credibility, and time.

Book a 15-Minute Consultation. No pressure. Just clarity.

👉 https://www.accountingatelier.com/law-firms

Final Word

You became an attorney to practice law—not to figure out how to reconcile trust ledgers or guess at compliance. Adopting a clear invoicing process fosters trust with clients and ensures accurate billing.

Let me handle your books like you handle your clients:

Precisely. Professionally. Without compromise.

Learn more about our service offerings here.