IOLTA Compliance for Law Firms: Common Mistakes and Best Practices

Every legal professional understands how critical it is to properly handle client funds, but maintaining IOLTA compliance can get complicated fast. An IOLTA account - Interest on Lawyers’ Trust Accounts - is designed to keep client money separate and safe, following strict rules set by each jurisdiction.

IOLTA programs direct the interest earned to fund civil legal services and legal assistance initiatives, making accurate trust management a public responsibility as well as a professional one.

Mishandling client IOLTA accounts isn’t just a paperwork mistake. It can trigger disciplinary action, damage your firm's reputation, or, in the worst case, lead to disbarment. Properly managing these accounts is a non-negotiable responsibility for firms of all sizes, from solo attorneys to smaller law firms.

The core requirement for IOLTA compliance is clear: never commingle client funds with the firm's business account, and maintain detailed, accurate records for every transaction. Each state or bar association sets specific IOLTA requirements and specific rules regarding deposits, withdrawals, and reporting, which makes a disciplined process for handling IOLTA transactions essential.

If you need a practical refresher, LawPay offers a helpful overview of managing IOLTA accounts and complying with modern financial institutions' expectations.

Profit & Loss and Trust Accounting: What Your Law Firm Is Really Earning

A profit and loss statement is meant to show what your law firm is actually earning, but accurate reporting depends on properly managing client IOLTA accounts. You must keep earned fees distinct from unearned balances held in the IOLTA trust account. Commingling these funds - even accidentally - leads to messy, misleading numbers that can throw off your firm's operating account reporting and violate IOLTA compliance requirements.

Risks of Mishandling Client Trust Accounts and IOLTA Compliance

Failing to maintain strict separation between client trust accounts and operating accounts exposes your firm to serious risk. Even a small slip - such as accidentally misusing funds or commingling client trust funds with the firm's operating account - can trigger bar complaints, audits, disciplinary action, and lasting damage to your reputation.

Why Business Funds Must Stay Separate from Trust Accounts

Law firms must maintain strict separation between business funds and trust account balances. Any co-mingling of operational revenue with client money creates immediate IOLTA compliance violations and exposes firms to audit risks and potential disciplinary action.

How Escrow Accounts Differ from IOLTA Trust Accounts

Escrow accounts are typically opened for specific transactions involving multiple parties, while IOLTA accounts pool smaller client deposits under one umbrella. Both require strict separation from business funds, but IOLTA accounts demand monthly reconciliation and compliance reporting under bar association rules.

Unlike a traditional escrow account tied to a specific transaction, an IOLTA account pools multiple client deposits under one structure. Law firms must never co-mingle business funds with trust balances, safeguarding compliance and preserving the interest generated for public legal aid programs.

Securing Your IOLTA Trust Account Against Audit Risk

Maintaining a properly titled IOLTA account is a fundamental requirement outlined by the American Bar Association. Firms must correctly label accounts, separate trust-held balances from business operations, and conduct monthly reconciliations to meet audit and fiduciary standards.

Common IOLTA mistakes like poor recordkeeping, mismanaging trust balances, or "borrowing" from trust accounts often lead to regulatory investigations and harsh penalties under state bar association rules. IOLTA accounts do not appear on your profit and loss statement until earned fees are properly transferred from the trust account to the firm's operating account.

Every Deposit and Disbursement Must Be Tracked Meticulously

Every deposit of trust fund deposits, every disbursement, and every IOLTA transaction must be tracked meticulously. Failing to properly manage IOLTA transactions risks mishandling other funds belonging to your clients - a risk no responsible attorney can afford.

Keeping track of every trust transaction - deposits, disbursements, and ledger adjustments - strengthens audit readiness and supports long-term compliance.

Safeguarding funds belonging to clients demands full reconciliation between trust accounts, operating accounts, and client ledgers each month.

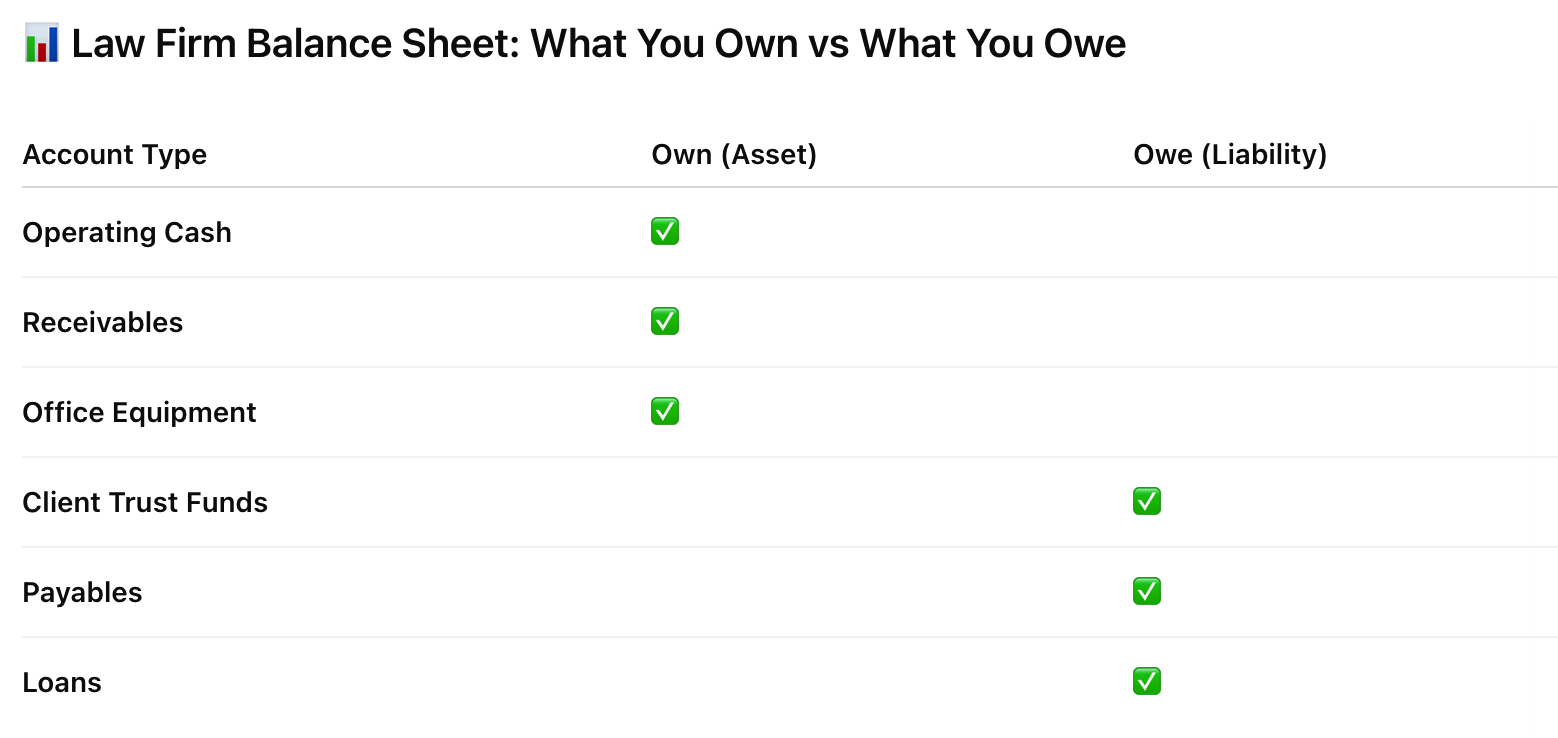

Balance Sheet and Trust Accounting: What You Owe vs. What You Own

Your law firm’s balance sheet provides a snapshot of its financial health at any given moment, laying out what you own and what you owe, side by side. Proper handling of client trust accounts and operating funds is critical to accurate reporting and IOLTA compliance.

Assets represent what the firm owns. Typical asset categories include:

Cash and operating accounts

Receivables from clients

Fixed assets like computers, desks, and office equipment

Liabilities are what the firm owes. These might be:

Unpaid vendor invoices

Outstanding loans or credit

Client funds sitting in trust accounts

It’s essential to keep operating cash and client trust funds completely separate. Money held in client trust accounts - including unearned client funds in IOLTA accounts - remains the property of the client and should always be listed as a liability. The firm’s business account cash belongs to the firm and appears under assets.

Law firms must classify operating cash, receivables, and office equipment as assets, while client trust funds, payables, and loans appear as liabilities on the balance sheet.

Learn more about maintaining accurate trust account balances through monthly three-way reconciliations.

Looking at both sides of the balance sheet helps you keep tabs on liquidity and keep firm and client money well apart. For firms, IOLTA accounts are always liabilities—those dollars are the client’s, not the firm’s. If you want to dig deeper, here’s a resource on trust account liabilities.

Cash Flow Statements and Trust Accounting: What You’re Actually Operating On

The cash flow statement shows the real movement of money - what’s coming in, what’s going out, and what’s left for daily operations. It focuses on your law firm’s business account and operating expenses, not client IOLTA accounts or client trust funds held in an IOLTA account.

Commingling is one of the fastest ways to distort financial records. If client trust funds are mixed with operating cash, your cash flow statement becomes unreliable, putting both financial reporting and IOLTA account compliance at risk. Keeping funds belonging to clients completely separate from the firm's operational accounts isn't just best practice - it’s critical protection.

Monthly three-way reconciliations are mandatory. They match the trust ledger, bank statement, and individual client ledgers to maintain accuracy. Skipping these reconciliations can cause discrepancies between reported cash flow and actual balances — creating compliance risks that affect your law firm's profitability and your ability to manage IOLTA account transactions properly.

Even small bookkeeping mistakes - like incomplete ledgers or skipped reconciliations - can distort a law firm's cash flow reports and threaten IOLTA compliance.

Proper trust account management requires structured oversight, monthly reconciliations, and client ledger precision - not casual bookkeeping. Specialized law firm bookkeeping services, like Accounting Atelier, proactively close these gaps before they escalate into compliance violations.

Why Accurate Client Ledgers Are Critical for IOLTA Compliance and Cash Flow Management

Every individual client ledger must be kept up to date. Failing to maintain accurate ledgers can distort your law firm’s cash flow statement, misrepresent your firm's business account position, and make forecasting difficult.

All IOLTA account and operating account activities must be documented meticulously. When recordkeeping falls behind, incomplete trust account records can mislead firm leadership, complicate account management, and trigger compliance concerns with the state bar association.

Maintaining a properly titled IOLTA account is a fundamental requirement outlined by the American Bar Association. Firms must correctly label accounts, separate client funds from business operations, and conduct monthly reconciliations to meet audit and fiduciary standards.

Without regular oversight, small discrepancies can quickly escalate into major trust accounting violations - jeopardizing your reputation, your financial standing, and your client trust obligations.

Strong cash flow management relies on precise reconciliation of IOLTA accounts, operating cash, and client-specific ledgers. For a more detailed view, explore how a properly maintained statement of cash flows supports law firm financial operations and compliance with IOLTA programs.

Accounts Receivable Aging and Trust Accounting: Why Law Firms Must Track by Matter

Tracking accounts receivable aging by matter, rather than overall, allows firms to spot overdue client payments faster and manage IOLTA accounts more accurately. Detailed aging reports help attorneys reconcile client trust accounts, monitor unearned client funds, and align collections with IOLTA account requirements.

When aging is tracked by matter, it becomes easier to match client billing, payment processing fees, and trust fund deposits in compliance with state bar association guidelines. This level of account management supports better cash flow forecasting, strengthens compliance oversight, and minimizes operating expenses tied to delayed collections.

Staying current with accounts receivable aging not only boosts collection rates, but also protects the integrity of IOLTA account records. It ensures attorneys manage client funds separately, follow IOLTA programs correctly, and maintain cleaner records for audits by financial institutions and legal aid offices when necessary.

Why Core Trust Accounting Reports Matter More Than Annual Tax Prep

Monitoring IOLTA accounts is a daily responsibility for law firms — not a once-a-year tax prep task. Waiting until year-end risks missing critical IOLTA compliance milestones, exposing the firm to audits, penalties, and mismanagement of client trust accounts.

The essential reports every firm must maintain for IOLTA account management include:

Three-way reconciliations

Detailed client ledger reports

Comprehensive bank statements from approved financial institutions

Each report plays a unique role. Three-way reconciliation immediately highlights discrepancies between client ledgers, trust balances, and bank statements. Client-focused reporting reinforces fiduciary responsibility by tracking unearned trust balances and maintaining client funds separate from the firm's business account.

Audit-ready documentation aligned with state bar association and IOLTA program guidelines ensures faster responses during IOLTA account audits. Maintaining accurate, transparent records protects the interest generated on IOLTA account balances and supports operational integrity for smaller law firms navigating compliance challenges.

For best practices, the American Bar Association provides a detailed trust accounting checklist to help firms uphold proper IOLTA requirements.

Why DIY Bookkeeping Fails IOLTA Account Compliance and Trust Fund Management

DIY bookkeeping tools can’t meet IOLTA account requirements or manage lawyer IOLTA accounts accurately. Incomplete reconciliation, missing documentation, and weak oversight of trust fund deposits and disbursements expose firms to major compliance risks.

Professional trust accounting generates critical reports, including:

Three-way reconciliations matching bank statements and client ledgers

Deposit client funds tracking and disbursement audits

Monthly IOLTA transactions reconciliation with financial institutions

Ledger reporting aligned with state bar association guidelines

Manual methods often miss interest earned on IOLTA account balances, fail to properly separate operating expenses, and neglect IOLTA program compliance. Law firms must maintain client funds separate from operational cash, using specialized legal accounting software to safeguard compliance and complete trust account corrections. Legal aid offices and regulators expect full audit trails - DIY systems rarely deliver at required standards.

Critical trust accounting reports like three-way reconciliations and audit trails require precision. DIY bookkeeping often falls short, exposing law firms to compliance risks.

Why It Matters:

Without consistently accurate reconciliations and automated client ledger management, law firms risk trust accounting violations. Specialized bookkeeping services, like those offered by Accounting Atelier, close these gaps before they turn into costly compliance problems.

Law firms depend on these reports for compliance and to support regulatory review. Without a professional structure, reconciliation can get unreliable, and that opens the door to error and discipline.

For advanced review of trust ledgers or historic trust account corrections, relying on experts just gives better results than any internal DIY method.

Law Firm Financial Infrastructure: Built for Compliance, Risk Protection, and Growth

Financial reporting isn't just accounting - it's operational control. For firms managing client trust accounts, structured financial systems are critical. Routine three-way trust reconciliations, client ledger oversight, and audit-ready statements aren't luxuries - they're non-negotiable foundations for IOLTA compliance and firm growth.

Accounting Atelier delivers IOLTA account management systems designed to align with state bar association regulations, safeguard entrusted client balances, and fortify your firm's operational integrity. From strategic trust account corrections to accurate interest earned tracking, our support ensures compliance isn't an afterthought - it's a competitive advantage.

Secure Your Financial Compliance Infrastructure and position your law firm for risk mitigation, stronger client confidence, and long-term scalability.

Attorney-Specific IOLTA Compliance FAQs

-

The most common error is failing to complete monthly three-way reconciliations. Without reconciling trust ledgers, bank statements, and client ledgers, discrepancies in IOLTA transactions can go unnoticed, risking serious compliance violations.

-

Firms must maintain a separate trust account at a qualified financial institution, distinct from the firm’s business account. Client funds should never be used for operating expenses and must be tracked through accounting software aligned with IOLTA guidelines.

-

Firms must maintain monthly three-way reconciliations, client ledger statements, detailed trust fund deposit records, and audit-ready reports in accordance with state bar association and IOLTA program standards.

-

Timely trust account corrections catch errors in trust fund deposits, disbursement tracking, and IOLTA transactions - helping firms accurately record interest earned before audits occur. Professional bookkeeping ensures funds belonging to clients are properly managed to meet IOLTA requirements.

-

DIY bookkeeping rarely captures the complexity of managing client funds, trust fund deposits, and interest generated on IOLTA accounts. A dedicated legal bookkeeping team ensures compliance with state bar association regulations and prevents financial mismanagement.